Category: Newsletters

ATO Debt Refinancing – Ask us, How?

If you have a large ATO debt and need to avoid a credit default, or you want to consolidate multiple debts, and you need to free up cash flow for your business, you might want to consider ATO debt refinancing.

Benefits of Refinancing your ATO Debt

You may be able to:

- Consolidate your tax debt into a single mortgage repayment;

- Avoid the ATO’s General Interest Charge (GIC), which is often higher than a home loan rate;

- Prevent credit defaults, as overdue ATO debt repayments can now be reported.

Refinancing to pay an Australian Taxation Office (ATO) debt, if the ATO will not extend terms, may be possible through specialist lenders using your property as security.

Speak to us about your refinancing options by calling us on (02) 8383 4466 and requesting a callback or making an appointment with the YML Finance Team.

How can YML help?

Talk to our YML Finance Team today to see how YML Group can assist you with your ATO debt refinancing. For more information, view our website and contact us on (02) 8383 4466 or by using our Contact Us page on our website

Trustee Distribution Resolutions – Don’t miss the 30 June Deadline

A well-prepared trustee distribution resolution for those of you who are currently operating a discretionary (family) or private trust helps support your taxation planning for the trust, as well as demonstrates good governance, helping to avoid costly disputes with the Australian Taxation Office (ATO).

What is a trust distribution resolution?

A trust distribution resolution is a trustee’s formal decision about how a trust’s financial year income will be distributed among its beneficiaries. This resolution ensures that beneficiaries become “presently entitled” to trust income. And this resolution is a part of the planned taxation strategy of any discretionary trust.

Why does a trust distribution resolution matter?

For Australian discretionary trusts and other private trusts, trustee distribution resolutions are one of the key documents that evidence trustee decisions. They help demonstrate that the trustee acted properly, in accordance with the trust deed and relevant tax law, and at the correct time.

Governance of a trust distribution resolution

It is important that a resolution complies with the trust deed, which sets out who may receive distributions, how the trust income is defined, the procedures for trustees to follow, and deadlines for trustees to meet. A resolution must operate within the trust deed’s rules; it may not override the trust deed’s rules.

Trustees should review their trust deed well before year-end, estimate trust income, determine proposed distribution of the estimated trust income, and ensure their resolution is properly documented and signed before 30 June 2026.

There are numerous and common mistakes made by trustees – when preparing their trustee distribution resolutions – which can lead to adverse taxation consequences:

- Missing the 30 June deadline

- Failing to comply with the trust deed

- Incorrectly dealing with capital gains or franked dividends

- Recording financial records incorrectly

- Not keeping minutes and evidence of a trustee’s decision-making

- Improperly executing resolutions, including no signature

If a trustee does not make a valid resolution by the due date, the consequences could be that the trust deed’s default provisions apply – and any new decisions made by a trustee are disregarded, or the trustee may be assessed on undistributed financial year income at the top marginal taxation rate.

Next Steps

Early planning of your trust distribution resolution can help mitigate taxation penalties and ensure your planned taxation strategy is underpinned by decisions made in the best interest of the trust and its beneficiaries.

As trust deeds vary, if you are a trustee, reach out to YML Chartered Accountants for advice specific to your trust.

Act now. Review your trust deed and prepare and sign your resolution before 30 June 2026.

How can YML help?

Talk to our YML Chartered Accountants today to see how YML Group can assist you with your 2026 trust distribution resolution. For more information, view our website and contact us on (02) 8383 4400 or by using our Contact Us page on our website

Incoming! Higher Superannuation Contribution Caps

Recent inflation and wage growth data released by the Australian Bureau of Statistics have confirmed that several important superannuation thresholds will increase from 1 July 2026. These changes will create opportunities for many of you to boost your retirement savings and might influence the timing of your future superannuation strategies.

Let’s look at the three main cap increases:

1. Transfer Balance Cap (TBC)

The increase in the General Transfer Balance Cap (TBC) from $2 million to $2.1 million represents the maximum amount of superannuation that can be transferred into the tax-free retirement phase. This latest increase follows previous adjustments in 2021, 2023 and 2025 as part of the indexation process.

For those of you who have not yet commenced a retirement phase pension by 1 July 2026, the full $2.1 million TBC will generally be available when you start drawing a retirement income stream. However, for those of you who have already commenced a retirement phase pension, only a partial increase might be received due to the proportional indexation rules that apply to personal TBCs.

If you have already fully utilised your personal TBC before 1 July 2026, you will not benefit from the increase at all. And those of you who are receiving a Transition to Retirement Income Stream (TRIS) need to understand what effect the conversion to retirement phase will have on any future TBC entitlement.

Those of you who are yet to start an account-based pension might wish to delay until after 1 July 2026, after first seeking professional financial advice.

The increase in the TBC also triggers increases to the two main superannuation contribution caps.

2. Concessional Contribution Cap

From 1 July 2026, the concessional contribution cap will rise from $30,000 to $32,500 each year. Concessional (before tax) contributions generally include employer superannuation guarantee contributions, salary sacrifice arrangements and personal contributions claimed as a tax deduction.

3. Non-Concessional Contribution Cap

From 1 July 2026, the non-concessional contribution cap will rise from $120,000 to $130,000 each year. Non-concessional (after tax) contributions are generally personal contributions made from after-tax money where no tax deduction is claimed.

The maximum Total Superannuation Balance (TSB) threshold determines eligibility for non-concessional contributions and the bring-forward contribution rules. If you were previously prevented from making further non-concessional contributions because of your superannuation balance exceeding the existing threshold, from 1 July 2026, you may be able to make additional after-tax contributions into your account.

However, caution is required for anyone considering triggering a bring-forward arrangement before 1 July 2026. Once a bring-forward period has commenced, the contribution limits and timeframes are locked in based on the rules that applied when it was triggered. This means if you are already in a bring-forward period, you will not benefit from the higher contribution caps or thresholds that commence from 1 July 2026.

Next Steps

With these major changes approaching – and the possibility of future legislative changes, ask us now at YML Super Solutions to review your SMSF strategy, especially if you want to make use of the bring-forward rule.

Decisions regarding pension commencements, contribution timing and bring-forward arrangements made over the next 12 months could have a substantial impact on your retirement savings opportunities.

How can YML help?

Talk to our YML Super Solutions Team today to see how YML Group can assist you with your SMSF. For more information, view our website and contact us on(02) 8383 4444 or by using our Contact Us page on our website

Australian Federal Budget 2026-27

On Tuesday 12 May 2026 the Treasurer Jim Chalmers handed down the 2026-27 Federal Budget, framing some of the more significant announcements as part of a broader plan to help young Australians access the property market.

While acknowledging that the key to housing affordability is supply, the Government clearly sees changes to negative gearing and the capital gains tax (CGT) discount as being important pieces in the housing affordability puzzle.

The Government has called this its most ambitious budget and if the proposed measures are implemented, the impact will be felt directly by a wide cross-section of Australian society, including individual taxpayers, investors, businesses, employers and those suffering from a disability.

The year’s budget has been released against a backdrop of significant economic challenges, including global fuel price shocks, persistent inflation, rising interest rates and growing concerns around housing affordability. These themes are reflected in the measures that have been announced by the Treasurer.

While the Government has announced some significant changes to the tax system, the superannuation system looks to have been left alone this year.

Key initiatives include:

Housing

- Changes to the tax system to reduce existing concessions for property investors.

- Extending the temporary ban on foreign purchases of established dwellings until 30 June 2029.

- An investment of $2 billion to help local governments and state utilities build infrastructure to support new housing.

Health

- Medicare Urgent Care Clinics will receive additional funding to ease the pressure on GPs and hospitals.

- Funds are allocated to list new medicines on the Pharmaceutical Benefits Scheme, including treatments for cystic fibrosis, kidney disease and various cancers.

- An additional $25 billion in funding for public hospitals.

- Reforms to the NDIS are expected to save $37.8 billion over the next four years. The scheme will be more focused on those with permanent and severe disabilities.

- Private health insurance subsidies for Australians over 65 are being cut, with savings being used to fund aged care and dementia care units.

Defence

- The defence budget will be increased by $53 billion over the next ten years

Fuel

- A $14.8 billion package will be used to help Australia strengthen fuel supply.

- A reduction in the fuel excise and heavy vehicle road user charge will continue to apply for three months from 1 April 2026

For further details, kindly click on the link below.

Budget 2026-27: Resilience and Reform

If we can assist you to take advantage of any of the Budget measures or to minimise your risk, you can reach us via email at contact@ymlgroup.com.au or by phone at (02) 8383 4400.

As always, we’re here if you need us!

Yoav Lewis

Chairman

Don’t want to pay Mortgage Lender’s Insurance? Check out the 95% First Home Buyer Scheme

Under an Australian government-backed initiative, eligible first home buyers can purchase a property with as little as a 5% deposit and without paying Lender’s Mortgage Insurance (LMI), which can add tens of thousands of dollars to the upfront cost of buying a home.

Why is there no need to pay LMI?

The 95% First Home Buyer Scheme was introduced to enable the government to guarantee up to 15% of a home loan, thereby reducing the lender’s risk and enabling first home buyers to avoid paying LMI.

To qualify, first home buyers must meet specific eligibility criteria, including property price threshold, and be an Australian citizen or permanent resident. The scheme is generally limited to those people who will purchase new and existing properties as owner-occupiers.

Thinking about buying your first home?

Speak to us to see if you’re eligible and how this scheme could work for you by calling us on (02) 8383 4466 and requesting a callback or making an appointment with the YML Finance Team.

How can YML help?

Talk to our YML Finance Team today to see how YML Group can assist you with your first property purchase. For more information, view our website and contact us on (02) 8383 4466 or by using our Contact Us page on our website.

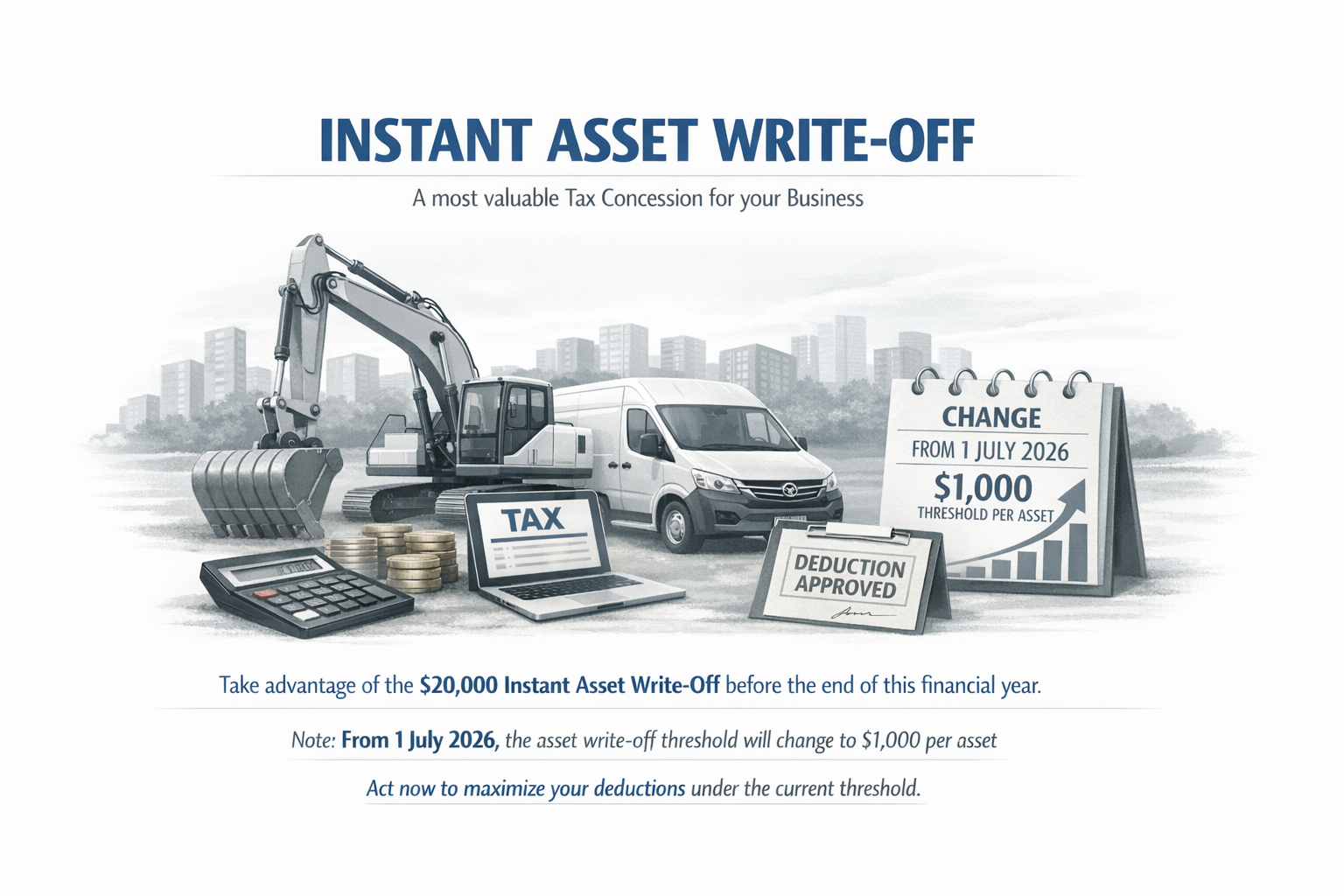

Instant Asset Write-Off – a most valuable Tax Concession for your Business before 1 July 2026 Threshold Change

For Australian small business owners, the Instant Asset Write-Off concession, used strategically, provides an opportunity to both claim a tax deduction and, equally, invest in their businesses.

The Australian Taxation Office (ATO) allows eligible Australian small businesses to immediately deduct the full cost of an asset under $20,000, rather than depreciating it over many years. This amount applies to each asset claimed, meaning unlimited multiple purchases may be written off in the same year. However, there are stipulations to follow to ensure compliance under the law.

To access the Instant Asset Write-Off, an Australian business must:

- Be actively carrying on a business, not just holding an ABN

- Have total aggregated turnover under $10 million

- Purchase new and or second-hand assets costing less than $20,000 each, GST-exclusive if registered for GST

- Ensure an asset is installed and in use by 30 June 2026

- Use an asset for a taxable business purpose, as only the business-use portion is claimable

Timing is Critical

The Instant Asset Write-Off threshold of $20,000 is currently legislated until 30 June 2026 with an expected significant drop to $1000 from 1 July 2026, unless the Australian government legislates an extension. Therefore, timing is critical for businesses who want to claim the write-off of their business asset purchases this financial year.

IMPORTANT!

Review planned assets for the next 12 months, bring forward any necessary purchases that align with your business’s needs, allow time for delivery and installation before 30 June 2026, and confirm your business’s eligibility to access the Instant Asset Write-Off concession.

How can YML help?

Talk to our YML Chartered Accountants today to see how YML Group can assist you with your Instant Asset Write-Off claims. For more information, view our website and contact us on (02) 8383 4400 or by using our Contact Us page on our website.

$100,000-plus Tax Deduction? Three Superannuation Strategies to implement NOW before 1 July 2026 Rule Changes

As 30 June 2026 approaches, you can take advantage of superannuation strategies still available under current rules that are due to change on 1 July 2026. This is the final year to use some deduction-friendly tactics and with some well-timed contributions before end-of-financial-year (EOFY), you can strengthen your retirement savings and receive some EOFY tax benefits.

These strategies must be implemented before 30 June 2026 to ensure that your contributions are received before the superannuation funds close off for the year, so early- to mid-June is your cut-off.

Maximise Concessional (Tax-Deductible) Contributions

People who use their concessional (tax-deductible) superannuation contributions up to the annual cap and follow the catch-up rule whereby the unused portions of the annual caps from the past five financial years can be added together, could claim $100,000-plus in tax deductions. If you have a starting balance of no more than $500,000 total in your superannuation account, you can effectively claim a consequential tax deduction using this concessional contribution strategy.

Therefore, if your total super balance is below the relevant threshold and you have not fully used some or all your concessional annual caps from the past five years, you may be able to make a larger tax-deductible contribution this year.

Concessional contributions are generally taxed at 15% with your superannuation fund which is much lower than most personal marginal taxation rates.

If you contributed, for example, $10,000 in a year when the annual cap was $27,500, you would have $17,500 unused, giving you the opportunity to contribute more than the standard annual cap this year ($30,000) and thus claim a larger tax deduction.

Factors including age eligibility, work test criteria, and lodgement of notices of intent must be met for this strategy to be implemented successfully. However, it remains one of the most tax-effective strategies for retirement savings growth.

Make Non-Concessional (After-Tax) Contributions

Considering making superannuation contributions from after-tax income can make a powerful impact on long-term wealth building.

Currently, superannuation rules allow an individual to contribute up to $120,000 per annum of after-tax income, which will increase to $130,000 from 1 July 2026, and up to three future years’ worth of contributions can be made at one time under the bring-forward rule.

For couples, this can mean contributing, if structured correctly and eligibility criteria is met, over $1 million of after-tax income into their superannuation accounts.

Co-Contribution Schemes

For people earning below $62,488 gross per annum, and who meet the eligibility criteria, the Australian government contributes up to $500 on up to $1000 of non-concessional (after-tax) contributions made by an individual into a superannuation account.

Additionally, if your spouse earns below $40,000 gross per annum, and eligibility conditions are met, an offset amount of up to $540 is claimable when you pay up to $3000 into your spouse’s superannuation account.

Downsizer Contribution Concession

If you have sold your owner-occupied, for at least 10 years, home and are aged over 55 years, you may be allowed to boost your superannuation account by an extra $300,000 in addition to any other contributions. This could be $600,000 for couples. It is worth seeking professional financial advice to ensure you follow the rules for this concession.

ACT NOW

This financial year is unlike any other in recent years due to the major superannuation reforms to commence on 1 July 2026. This is your last chance to use several contribution strategies to boost your retirement savings.

If you are unsure how much you can contribute or which strategy is right for you, seek advice from YML Group. Acting now can deliver both immediate tax-deductions and long-term financial growth.

How can YML help?

Talk to our YML Super Solutions Team today to see how YML Group can assist you with your superannuation contributions. For more information, view our website and contact us on (02) 8383 4444 or by using our Contact Us page on our website.

The Invisible Bill: 5 surprising Truths about your Land Tax Valuation

Land tax is a significant cost to Australian property owners, yet few people understand how their land valuation is calculated for the purpose of land tax. Land tax assessments are undertaken by the Australian government, specifically by each state’s Valuer-General, using large-scale valuation systems.

Historically, property-based taxation was based on valuation systems that were surprisingly transparent to property owners, such as counting chimneys for the Hearth Tax or windows for the Window Tax. Today’s methods are less visible due to the digital age of fact-finding.

We outline five truths about the assessment process used to determine your land value:

|

1. Unimproved Value of Land 2. Top-Down Estimate 3. Mass Appraisal To value millions of properties each year, the Valuer-General relies on a mass appraisal method of valuation. Properties in similar locations and zoning categories are grouped together, and a ‘benchmark property’ is selected for a detailed valuation, thereby creating a percentage change applied to every other property in the group. There is a mathematical error if your property is unique due to its features and characteristics – easements, steep terrain, access limitations, for example – that are not identical to the benchmark. 4. Legal Restrictions Land valuation is normally based on the concept of “highest and best use”, that is, the most profitable use allowed under zoning rules, however certain legal restrictions can override this principle. For example, a legal case in 2023 involving the Sydney Fish Market highlighted how land subject to a Crown lease must be valued on the permitted use defined in the lease and not on the most profitable use allowed under zoning rules. The court disagreed that the site could be developed into luxury apartments because the lease restricted the site’s use to a “wholesale fish market”, resulting in the land valuation being adjusted lower than if the “highest and best use” rule was applied. Legal restrictions can significantly affect valuation if there is an overriding factor permitting use of the land in a context that would increase or reduce the land value. 5. Unfairness will not win an Objection A property owner who wishes to challenge a land tax valuation based on it being ‘unfair’ is in for a rude awakening. When objecting to a land tax assessment, successful applications require evidence, not just dissatisfaction or general grievance. Commonly, reliable evidence may be:

Strict timeframes apply to challenging a land tax valuation. A property owner has no more than 60 days from the notice date to lodge an objection application. |

Land Valuation Notice – What to do NEXT

If you have received a land valuation notice, it would be prudent to review the details of it carefully. Because the burden of proof lies with you, the property owner, you must decide if you have identified if the Valuer-General has truly understood your property in their assessment of it. If you want to have their assessment reviewed, do you have evidence?

YML Group can review your Land Tax assessment and help you determine whether lodging an objection application with Revenue NSW might be a worthwhile step for you to take to mitigate your Land Tax obligation.

How can YML help?

Talk to our YML Chartered Accountants today to see how YML Group can assist you with your Land Tax obligation. For more information, view our website and contact us on (02) 8383 4400 or by using our Contact Us page on our website.

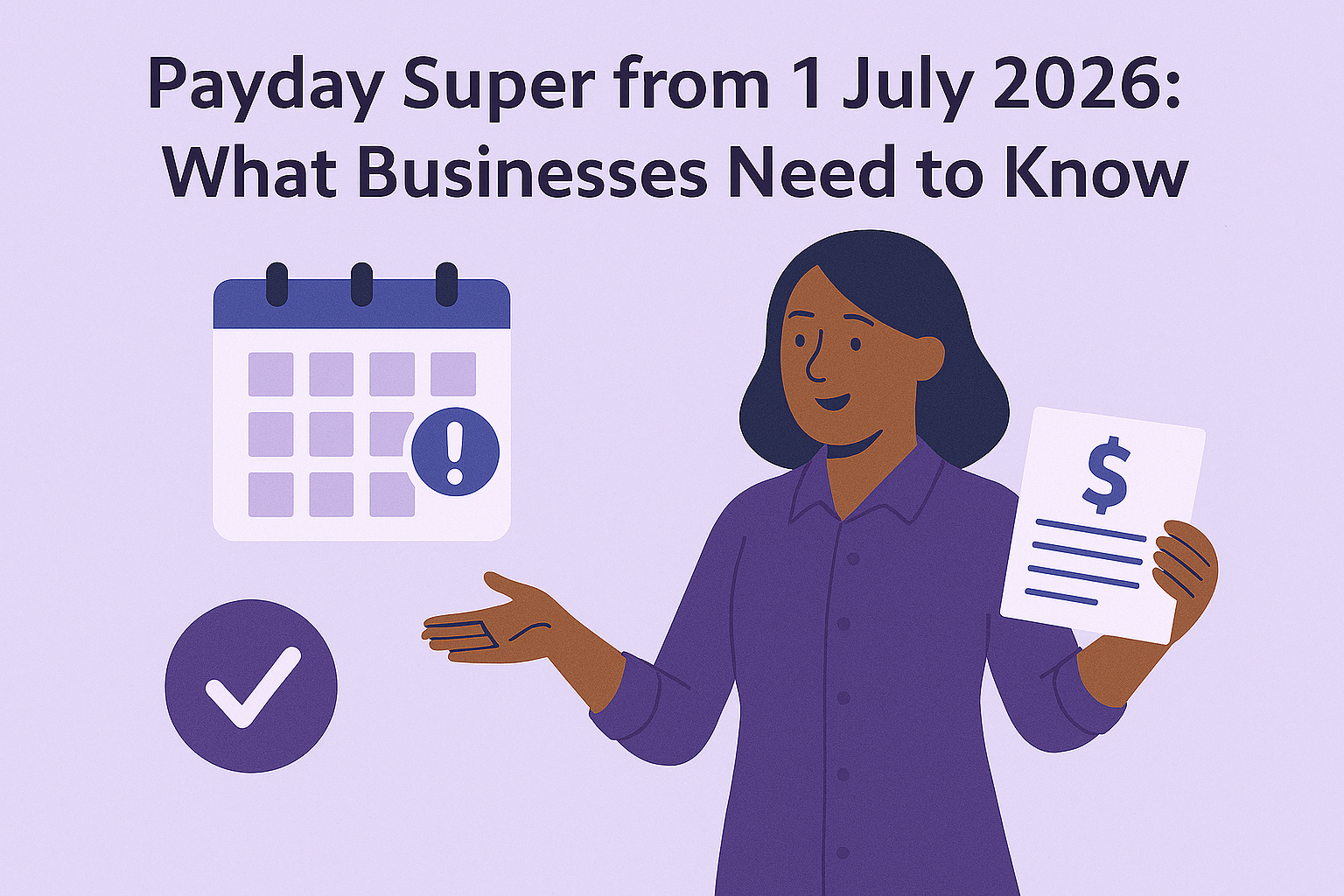

Payday Super from 1 July 2026: What Businesses Need to Know

Australia’s superannuation system, notably the current quarterly payment cycle, will change for employers and employees from 1 July 2026. Employers’ superannuation guarantee (SG) contributions will need to align directly with the payroll cycle, meaning that the SG will be paid at the same time as wages and salaries. This change is known as ‘Payday Super’.

Changing the SG payment cycle gives regulators a way to tackle the growing issue of unpaid or underpaid SG by providing clearer visibility of employer compliance.

How does Payday Super benefit employees?

This reform aims to improve transparency for employees. It will ensure that SG is received sooner than quarterly, more consistently, and help boost retirement savings outcomes.

What are the implications for businesses?

Payday Super represents a significant shift in payroll and cash flow management for many businesses. Specifically, businesses will no longer have the flexibility to hold SG contributions until the end of the quarter.

Under the new rule, starting on 1 July 2026, employers will be required to:

- Calculate SG on or before each payday

- Pay SG at the same time as wages and salaries, be it weekly, fortnightly or monthly

- Ensure payroll systems are configured to process SG automatically with wages and salaries

This shift to more frequent SG payments will see the need for:

- Cash flow management to be adjusted more frequently

- Payroll processes and systems to be updated, if needed, to ensure real-time calculations and reporting of the SG

- SG payment error identification and corrections to be made more readily, thus mitigating the risk of late or missed payment penalties

Preparing your Business early will be key to successfully transitioning to Payday Super

YML Group can support you with the approaching introduction of Payday Super. NOW is the ideal time for you to review your payroll system and cash flow management.

Our YML Business Services Team has the expertise to assist you with:

- Reviewing and possibly updating your payroll setup to accommodate the alignment of SG payments with earnings payments

- Assessing the impact of Payday Super on your cash flow

- Planning for more frequent SG outflows from your cash flow

- Ongoing maintenance of your payroll setup to avoid unnecessary disruption to your business as the new rule comes into effect on 1 July 2026

Contact YML Group today to discuss how we can make the introduction of Payday Super an easier transition for your business and you.

How can YML help?

Talk to our YML Business Services Team today to see how YML Group can assist you with your SG obligations. For more information, view our website and contact us on (02) 8383 4455 or by using our Contact Us page on our website.

Did you know you can buy an investment property using home loan interest rates?

If you’re interested and would like to explore whether this option could work for your situation, please feel free to give us a call. We’re more than happy to discuss the details and answer any questions you may have.

How can YML help?

Talk to our YML Finance Team today to see how YML Group can assist you with SMSF property purchases. For more for more information, view our website and contact us on (02) 8383 4466 or by using our Contact Us page on our website.