Author: Yml Yml

The Invisible Bill: 5 surprising Truths about your Land Tax Valuation

Land tax is a significant cost to Australian property owners, yet few people understand how their land valuation is calculated for the purpose of land tax. Land tax assessments are undertaken by the Australian government, specifically by each state’s Valuer-General, using large-scale valuation systems.

Historically, property-based taxation was based on valuation systems that were surprisingly transparent to property owners, such as counting chimneys for the Hearth Tax or windows for the Window Tax. Today’s methods are less visible due to the digital age of fact-finding.

We outline five truths about the assessment process used to determine your land value:

|

1. Unimproved Value of Land 2. Top-Down Estimate 3. Mass Appraisal To value millions of properties each year, the Valuer-General relies on a mass appraisal method of valuation. Properties in similar locations and zoning categories are grouped together, and a ‘benchmark property’ is selected for a detailed valuation, thereby creating a percentage change applied to every other property in the group. There is a mathematical error if your property is unique due to its features and characteristics – easements, steep terrain, access limitations, for example – that are not identical to the benchmark. 4. Legal Restrictions Land valuation is normally based on the concept of “highest and best use”, that is, the most profitable use allowed under zoning rules, however certain legal restrictions can override this principle. For example, a legal case in 2023 involving the Sydney Fish Market highlighted how land subject to a Crown lease must be valued on the permitted use defined in the lease and not on the most profitable use allowed under zoning rules. The court disagreed that the site could be developed into luxury apartments because the lease restricted the site’s use to a “wholesale fish market”, resulting in the land valuation being adjusted lower than if the “highest and best use” rule was applied. Legal restrictions can significantly affect valuation if there is an overriding factor permitting use of the land in a context that would increase or reduce the land value. 5. Unfairness will not win an Objection A property owner who wishes to challenge a land tax valuation based on it being ‘unfair’ is in for a rude awakening. When objecting to a land tax assessment, successful applications require evidence, not just dissatisfaction or general grievance. Commonly, reliable evidence may be:

Strict timeframes apply to challenging a land tax valuation. A property owner has no more than 60 days from the notice date to lodge an objection application. |

Land Valuation Notice – What to do NEXT

If you have received a land valuation notice, it would be prudent to review the details of it carefully. Because the burden of proof lies with you, the property owner, you must decide if you have identified if the Valuer-General has truly understood your property in their assessment of it. If you want to have their assessment reviewed, do you have evidence?

YML Group can review your Land Tax assessment and help you determine whether lodging an objection application with Revenue NSW might be a worthwhile step for you to take to mitigate your Land Tax obligation.

How can YML help?

Talk to our YML Chartered Accountants today to see how YML Group can assist you with your Land Tax obligation. For more information, view our website and contact us on (02) 8383 4400 or by using our Contact Us page on our website.

Payday Super from 1 July 2026: What Businesses Need to Know

Australia’s superannuation system, notably the current quarterly payment cycle, will change for employers and employees from 1 July 2026. Employers’ superannuation guarantee (SG) contributions will need to align directly with the payroll cycle, meaning that the SG will be paid at the same time as wages and salaries. This change is known as ‘Payday Super’.

Changing the SG payment cycle gives regulators a way to tackle the growing issue of unpaid or underpaid SG by providing clearer visibility of employer compliance.

How does Payday Super benefit employees?

This reform aims to improve transparency for employees. It will ensure that SG is received sooner than quarterly, more consistently, and help boost retirement savings outcomes.

What are the implications for businesses?

Payday Super represents a significant shift in payroll and cash flow management for many businesses. Specifically, businesses will no longer have the flexibility to hold SG contributions until the end of the quarter.

Under the new rule, starting on 1 July 2026, employers will be required to:

- Calculate SG on or before each payday

- Pay SG at the same time as wages and salaries, be it weekly, fortnightly or monthly

- Ensure payroll systems are configured to process SG automatically with wages and salaries

This shift to more frequent SG payments will see the need for:

- Cash flow management to be adjusted more frequently

- Payroll processes and systems to be updated, if needed, to ensure real-time calculations and reporting of the SG

- SG payment error identification and corrections to be made more readily, thus mitigating the risk of late or missed payment penalties

Preparing your Business early will be key to successfully transitioning to Payday Super

YML Group can support you with the approaching introduction of Payday Super. NOW is the ideal time for you to review your payroll system and cash flow management.

Our YML Business Services Team has the expertise to assist you with:

- Reviewing and possibly updating your payroll setup to accommodate the alignment of SG payments with earnings payments

- Assessing the impact of Payday Super on your cash flow

- Planning for more frequent SG outflows from your cash flow

- Ongoing maintenance of your payroll setup to avoid unnecessary disruption to your business as the new rule comes into effect on 1 July 2026

Contact YML Group today to discuss how we can make the introduction of Payday Super an easier transition for your business and you.

How can YML help?

Talk to our YML Business Services Team today to see how YML Group can assist you with your SG obligations. For more information, view our website and contact us on (02) 8383 4455 or by using our Contact Us page on our website.

Did you know you can buy an investment property using home loan interest rates?

If you’re interested and would like to explore whether this option could work for your situation, please feel free to give us a call. We’re more than happy to discuss the details and answer any questions you may have.

How can YML help?

Talk to our YML Finance Team today to see how YML Group can assist you with SMSF property purchases. For more for more information, view our website and contact us on (02) 8383 4466 or by using our Contact Us page on our website.

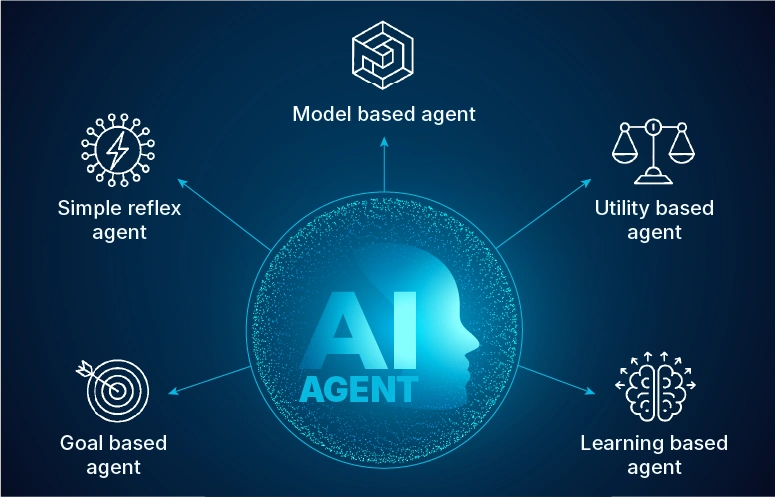

Beyond ChatGPT: Why Custom AI Agents Are the Next Evolution in Workflow Automation

From Conversation to Action: How YML Group is Deploying AI That Seamlessly Integrates Within Your Systems

If your team is using ChatGPT, Claude, or other LLM tools, you've likely experienced the productivity boost they provide. But you've also probably hit their limitations: copying and pasting between systems, manually transferring information, and watching AI-generated insights sit unused because they're disconnected from your actual workflows.

At YML Group, we're moving beyond conversational AI to deploy custom AI agents that integrate seamlessly into business operations – and we're implementing them internally first.

The Difference Between AI Tools and AI Agents

Out-of-the-box LLM subscriptions are powerful for:

- Drafting content and emails

- Answering questions

- Analysing data you manually provide

- Ideation and brainstorming

Custom AI agents integrated within business processes extend these capabilities by:

- Connecting directly to your data ecosystem — integrating with internal and external data sources including CRM platforms, databases, knowledge bases, and core business systems to access real-time information

- Making smarter decisions over time — analysing data patterns, learning from outcomes, and progressively improving recommendations and actions based on your business results

- Taking action without manual intervention — executing tasks autonomously on your behalf through secure API integrations, from updating records to triggering workflows

- Embedding into your existing processes — operating as a native part of your workflows rather than requiring you to switch between tools or manually transfer information

- Adapting to your unique operations — learning from your specific business context, industry terminology, compliance requirements, and operational rules to deliver tailored results

- Orchestrating complex workflows — automating entire multi-step processes end-to-end, coordinating tasks across systems and team members without human oversight

Think of a custom AI agent as a tireless team member who inherently understands your systems, has instant access to your data, operates with your business logic, and executes tasks autonomously while you focus on strategic work.

Walking the Walk: YML's Internal AI Implementation

At YML, we practice what we preach. We've examined multiple accounting operations that drive our business and are building AI agents to improve internal operations, reduce manual errors, and increase the quality of services we deliver to you.

Use cases we're currently implementing:

Improving Process Efficiency

- Automate job workflow management by intelligently routing tasks and tracking status

- Optimise delivery schedules by analysing workload balance, proactively identifying bottlenecks, and devising mitigation strategies to reduce risk

- Handle document collection and ingestion by monitoring email inboxes, extracting relevant financial documents, categorizing them by client and type, and preparing them for processing

Reducing Errors

- Pre-process financial data by analysing documentation, extracting key information, and structuring it for review

Improving Customer Interaction

- Generate draft communications to clients regarding missing documentation, status updates, and routine inquiries based on current job status

These use cases represent the kind of transformation we see as possible across professional services: turning hours of manual coordination and data entry into automated processing, freeing teams to focus on higher-value advisory work and complex problem-solving.

Our Approach: Built for Your Business

- Understand your business-specific pain points and overall aspirations

- Define specific, tangible objectives aligned to your organizational roadmap (ensuring adoption)

- Approve use cases and sequence of implementation

- Assess your systems landscape and align a solution architecture that fits your technology stack

- Design and approve the solution

- Integrate data sources securely

- Develop and train the AI agent

- Test thoroughly in controlled environments

- Manage change through education, training, and clear communication

- Deploy in a phased approach

- Continuously improve by monitoring performance, refining training, innovating, and deploying enhancements

Ready to Explore What's Possible?

If your team is ready to move to AI agent-enabled workflows, we'd love to discuss your current challenges and future aspirations.

We're building this future for ourselves at YML Group, and we're ready to build it with you.

Want to learn more? We're offering complimentary workflow assessments to explore where AI automation could deliver the most value for your organization.

Contact us to schedule your assessment and discover how custom AI agents can transform your operations.

How can YML help?

- Avi Sharabi

- CEO – YML AI

- M: 0410 348 297 ·

- E: Avi.Sharabi@ymlgroup.com.au

- W: www.ymlgroup.com.au

Could you purchase a Property for your SMSF?

A SMSF with around $250,000 could potentially give you enough to cover your setup and ongoing compliance costs, provide a deposit for a property and maintain liquidity for fees and future diversification.

Buying a property for your SMSF has its pros and cons. We outline them here:

PROS

Tax advantages:

- Rental income is generally taxed at 15% which is often lower than your personal marginal tax rate

- Capital gains tax (CGT) on property held longer than 12 months is effectively 10%

- Once you enter pension phase, both rental income and CGT can become tax-free

Borrowing leverage:

- SMSFs can use Limited Recourse Borrowing Arrangements (LRBAs) to buy property, enabling you to buy a larger asset than your SMSF balance alone would allow

Rental income boosts your SMSF:

- Rent paid by tenants goes directly into your SMSF

- Commercial property can be leased to your own business at market rates

Long-term capital growth:

- Growth of a property asset inside a SMSF is magnified by concessional tax treatment

CONS

Tight Australian Taxation Office (ATO) compliance:

- Mistakes can be costly

Less flexibility:

- Property ties up a large part of your SMSF, making diversification harder

Loan restrictions:

- SMSF loans often have higher interest rates and stricter conditions

No personal use:

- Your family and you may not live in or use a property bought for your SMSF

Learn more about how we can help you by calling us on (02) 8383 4466 and requesting a callback or making an appointment with the YML Finance Team.

How can YML help?

Talk to our YML Finance Team today to see how YML Group can assist you with SMSF property purchases. For more information, view our website and contact us on (02) 8383 4466 or by using our Contact Us page on our website.

Challenging the Valuer-General’s Valuation of your Land

Australian landowners often assume a land valuation is final, but many assessments can be successfully disputed. Land Tax is one of the key property-related obligations in Australia, and it is based on a valuation undertaken by the Valuer-General who does not typically visit every property to ascertain unique features. Therefore, you might have cause to challenge the Valuer-General’s assessment.

The Valuer-General relies heavily on a mass-appraisal method, which prioritises efficiency over site-specific accuracy. This Mass Valuation model often means that individual blocks of land are not assessed with consideration for a block’s attributes and constraints.

Mass-appraisal uses the recent sales of chosen ‘benchmark’ properties – based on location, zoning and land use – to calculate a one-size-fits-all percentage change in valuation; and assumes a valuation of vacant land at its ‘highest and best use’.

This method is efficient – it assumes your property is identical to the ‘benchmark’, but it does not reflect those attributes – easements, environmental factors such as contamination, topography such as steep slopes, restrictive overlays such as heritage limitations, among others – which are not shared by grouped ‘benchmark’ properties.

What this means for you

Mass Valuation could give you valid grounds for an objection to a land tax liability that you deem to exceed your land’s individual valuation. However, to succeed, an objection must show a quantifiable error such as:

- Incorrect market value (at the valuation date)

- Wrong land size, boundaries, or zoning restrictions

- Incorrect parcel apportionment

- Failure to consider constraints (including limited ‘highest and best use’ for vacant land)

How to build a strong objection

You may not object simply because your Land Tax liability has increased. You may object if there is a mathematical error.

Strong objections use legal discovery to report errors, and ensure the following:

- Comparable sales evidence – at least three (3) similar sales around the valuation date and adjusted to reflect land-only value

- Documented site-specific disadvantages – constraints identified that the mass-appraisal missed

- Timely lodgement of objection – within 60 days from the date of notice

Examples of successful challenges

Australian courts have repeatedly overturned Valuer-General-assessed valuations when assumptions under the mass-appraisal method fail.

Here are some recent Australian court decisions which show how land valuations can be dramatically reduced when constraints are considered, instead of ignored or misinterpreted:

- Hammock Investments (NSW):

o Environmental limits reduced value from $8M to $810k - Perisher Blue (NSW):

o National Park lease restrictions cut value from $39M to $14M - WSTI Properties (VIC):

o Heritage overlay reduced value from $6.2M to $2.925M - Goldmate Property (NSW):

o Compulsory acquisition value increased from $0 to $9.5M after zoning errors were corrected

Lodging an objection and requesting a reassessment can result in significant savings for Australian landowners.

It is important to seek property valuation advice and prepare evidence for an appeal, but an objection can be an effective strategy for paying less Land Tax.

Next Steps

YML Group can review your Land Tax liability and help you determine whether lodging a dispute with Revenue NSW might be a worthwhile step for you to take to mitigate your Land Tax obligation.

How can YML help?

Talk to our YML Chartered Accountants today to see how YML Group can assist you in your Land Tax obligation. For more information, view our website and contact us on (02) 8383 4400 or by using our Contact Us page on our website.

Introducing YML Group’s New Live Q&A Online Feature

YML Group’s new Live Q&A online assistant is driving the next step in our digital transformation. We are moving confidently into the Artificial Intelligence (AI) era, committed to strengthening our AI offering to you and enhancing your online experience with YML Group.

Introducing our Live Q&A online assistant on our YML Group website, you will find this intelligent, AI-powered tool is designed to provide you with instant answers, streamlined interaction with us and a more intuitive, responsive digital experience.

You will engage with our smart virtual assistant through a conversational, easy-to-use interface, whether you are looking for information about our services, have a question, or simply want to explore and browse our offers. Our virtual assistant is available anytime to guide you, and is a faster, more convenient way to connect with us.

We have a mission to remain at the forefront of technology and to continue to modernise how we serve you and our broader community.

Our Invitation to You

We invite you to now visit our website – www.ymlgroup.com.au/ai – and try out our new Live Q&A online feature. Please enjoy this dynamic and fresh digital enhancement to our important and valued customer service.

How can YML help?

Talk to our YML Chartered Accountants today to see how YML Group can assist you with our new Live Q&A. For more information, view our website and contact us on (02) 8383 4400 or by using our Contact Us page on our website.

What Australia’s recent Age Pension and Deeming Changes mean for your Retirement

Important updates came into effect on 20 September 2025 that may influence the Age Pension entitlement or eligibility for key senior concessions. Recipients of the Age Pension and self-funded retirees may be impacted by four key changes:

1. Deeming Rate Increases

The most significant change is a 50-basis point rise in deeming rates used by Centrelink in the income means test.

Deeming rates are a notional or ‘assumed’ income rate applied to financial assets. Using a deeming rate is a simple way for the Australian Taxation Office (ATO) to calculate income without needing to track actual investment returns.

Deeming rates have been frozen for the past five years as part of the COVID-19 response. This increase is an adjustment to reflect current market conditions more accurately, even though interest rates may be easing.

New deeming rates from 20 September 2025:

Low deeming rate increases from 0.25% to 0.75%; and

the higher (standard) deeming rate will increase from 2.25% to 2.75%.

The low rate applies to the first $64,200 of financial assets for a single pensioner and the first $106,300 for a pensioner couple. Any amount above these thresholds is deemed at the higher rate.

As an increase in the deeming rate means more income is deemed to have been earned from financial assets, this will generally lead to a reduction in the Age Pension. For every $1,000 of financial assets, a fortnightly Age Pension could decrease by $2.50.

2. Age Pension Increase

The maximum Age Pension amount will increase, providing a boost to all pensioners.

New maximum fortnightly payments from 20 September 2025:

For a single pensioner, there will be an automatic increase of $29.70 to $1,178.70; and

for a pensioner couple, there will be an automatic increase of $44.80 to $1,777.00 ($880.50 each).

3. Part-Pension Cut-Off Limits Rise

The maximum income you may earn before losing eligibility for a part Age Pension has been raised. This is a direct result of the increase to the Age Pension.

New fortnightly cut-off limits are:

For a single pensioner, an increase of $59.40 to $2,575.40; and

for a pensioner couple, an increase of $89.60 to $3,934.00 (combined).

4. Commonwealth Seniors Health Card (CSHC) Income Limits Rise

Self-funded retirees who do not qualify for the Age Pension may benefit from this valuable card which provides access to cheaper medicines and other state-based concessions.

New annual income limits for CSHC are:

For a single person, an increase of $2,080 to $101,105; and

for a couple, an increase of $3,328 to $161,768 (combined).

TIP: If your income was previously just above the old limit, you should consider applying for the CSHC. Notably, the CSHC has no assets test, making it particularly beneficial for retirees whose assets disqualify them from the Age Pension.

Next Steps

Before jumping into implementation of any financial strategy, speak to a financial adviser about your personal circumstances to ensure decisions are made that align with your retirement objectives.

How can YML help?

Talk to our YML Financial Planning today to see how YML Group can assist you with your retirement entitlements. For more information, view our website and contact us on (02) 8383 4444 or by using our Contact Us page on our website.

Are you paying too much Land Tax?

Land Tax in New South Wales is an annual charge on the ownership of land (property), calculated as at midnight on 31 December each year.

The NSW Valuer-General assesses and determines the unimproved land value, and the tax is calculated using the average of the current and previous two years’ values to account for fluctuations.

It is payable by individuals, companies and trustees who own taxable property, although exemptions may apply. Common exemptions include a principal place of residence, primary production land, and property used for charitable purposes.

Early in each new calendar year, valuation assessments are issued, and landowners are generally required to pay their Land Tax obligation within 30 days. Instalment plans can be arranged, but there are penalties, such as interest payments and or debt collection, for failure to pay on time.

What to do if you believe your Land Tax liability is too much?

If you deem a Land Tax assessment is incorrect or is unexpectedly too high, you may challenge the Valuer-General’s land value of your property by lodging an objection with the Australian Taxation Office (ATO).

Lodging an appeal and requesting a reassessment can result in significant savings for landowners. Some successful challenges have been based on errors in comparable sales, zoning assumptions, and incorrect treatment of the land’s ‘highest and best use’ in relation to market value.

It is important to seek property valuation advice and prepare evidence for an appeal, but an objection can be an effective strategy leading to a reduced Land Tax liability.

Next Steps

YML Group can review your Land Tax liability and help you determine whether an appeal to the ATO might be a worthwhile step for you to take to mitigate your Land Tax obligation.

How can YML help?

Talk to our YML Chartered Accountants today to see how YML Group can assist you in your Land Tax obligation. For more information, view our website and contact us on (02) 8383 4400 or by using our Contact Us page on our website.

Personal Residential Property Asset Acquisition for your SMSF

The question: Can our SMSF acquire a residential property from us personally? requires a follow-up question: How is the property used?

Before answering these questions, you will require an explanation of Business Real Property (BRP) which is defined under Section 66 of the Superannuation Industry (Supervision) Act 1993 as “any freehold or leasehold interest in real property where the property is used wholly and exclusively in one or more businesses.”

This definition hinges on use, not the type or zoning of the property, and the Australian Taxation Office (ATO) clarifies that even a property that looks ‘residential’ can qualify as BRP if it is genuinely used in the operation of a business. Conversely, a commercial property might not quality as BRP if it is partly used for private purposes.

Therefore, under section 66, a property’s eligibility as BRP depends entirely on its current use in a genuine business operation, not on its appearance or zoning.

If a property satisfies the BRP test, it can be acquired by an SMSF from a related party — provided the transaction occurs at market value.

This allows business owners to transfer premises used in their business into their SMSF, helping free up capital while retaining operational control through a lease arrangement.

However, if the property is not wholly and exclusively used in a business, section 66 prohibits the transfer, and a SMSF might risk breaching the Superannuation Industry (Supervision) Act 1993.

Section 66 Exemption - Examples

The exemption under Section 66 is tested at the time of acquisition. If a property is used, for example, by a doctor, accountant or dentist, 100 per cent of the time for their business with no residential purpose, then the property would be classified as BRP and may be acquired from a related party to a SMSF.

However, if, for example, a property is a working farm that has a farmhouse used residentially, then the farmhouse portion could be considered incidental, and the property may also be acquired from a related party to a SMSF.

Furthermore, a motel that has a manager’s quarters within the property could also be considered incidental, and the property may also be acquired from a related party to a SMSF.

Next Steps

If you are considering a property transaction involving a SMSF and a related party, it is essential to assess the property's current and intended use — not just its type or zoning. Would you like help evaluating a specific property scenario? Ask us at YML Super Solutions to look more closely at the exact details of a property’s use for your SMSF strategy.

How can YML help?

Talk to our YML Super Solutions Team today to see how YML Group can assist you with your SMSF. For more information, view our website and contact us on (02) 8383 4444 or by using our Contact Us page on our website.